Published December 29, 2025

Ideas In the Mix

Here, various items that are on my mind, positions that perhaps don’t command a full treatment, all to give you some sense of my thought process and perhaps some things you might consider for yourself.

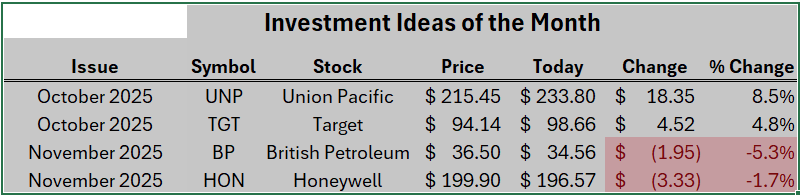

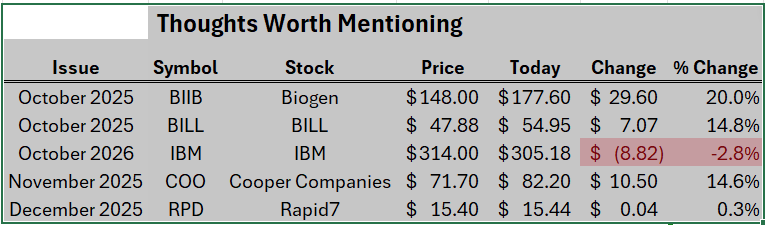

Last month we mentioned several in Thoughts Worth Mentioning so we’ll start with an update on whatever is worth commenting on since last month. First, a simple scorecard:

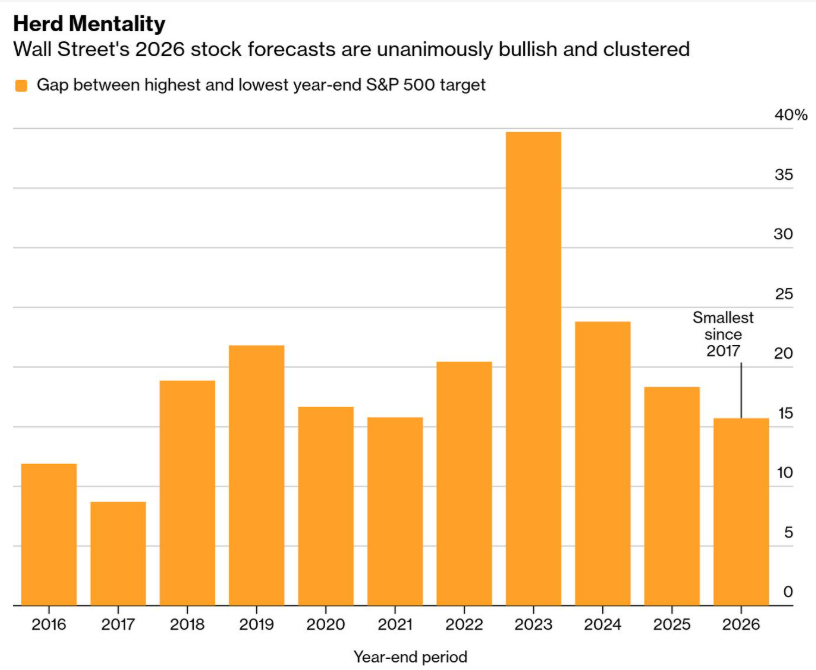

Below, the Contrarian in me is itchy. There is a consensus and while it provides money for the bull move, unanimity is hardly something to seek in your investment analysis. Just be aware of this.

What happened in 2018? Market down 4% but the 4Q move was a negative 14%. This whole consensus thing is tempering my risk taking, so you know.

BILL $55.00

Symbol BILL

Stock is now ‘in play’ with activists active. $47.88 when I first mentioned it, up 15% since. As a result, I increased my position by 60% and it’s now 6% of my trading account. I check news frequently on it. I will stay at 6% exposure until the situation resolves, one way or the other. If you do not yet own the stock, I would not buy it at this juncture. The increase has shifted the risk-reward relationship.

IBM

Symbol IBM $305

Stock really hasn’t moved a lot, just waffling back and forth. No real news of major import. My second largest position, 7% of my trading account.

Target

Symbol TGT $98.74

Note Important News on Target piece this month.

October investment of the month.

First, a valuation summary, showing that this stock really is cheap relative to its history:

Price has fallen 65% since 2021, thus pushing its valuation metrics ever lower. Its P/Sales ratio down to 0.4x versus a five-year average of nearly 0.7x. The P/E ratio is 11 compared to a long-term average of 16. And the P/Book ratio is currently 2.7 compared to a five-year average of 5.2. Target’s roughly 5% dividend yield is near the highest levels in its history. Target’s stock looks cheap.

New CEO takes the helm in February but clearly he is not waiting…we just got this which validates to me the company is moving off the dime and IMO, headed in the right direction. This is fun:

https://finance.yahoo.com/news/target-opens-target-soho-design-110100302.html

Biogen

Symbol BIIB $177

Continued slow and steady movement forward on their drug pipeline and development, up nearly 20% since recommended.

Leqembi (lecanemab) – Alzheimer’s Disease

Skyclarys – Friedreich’s Ataxia

Zurzuvae – Postpartum Depression

The company is positioning these new drugs to offset declining revenues from older MS products facing biosimilar competition. 8% of my trading account at notional values (the actual strike price of the call options I’m long assuming they are exercised). Actual cash outlay at cost of 2% of account value.

Careful! Stocks like this are prone to serious volatility on good or bad news on drug development. It’s why with biotech or similar high vol stocks, I prefer to buy long-dated call options instead of the stock, although here, I have both. The Jan 2027 series look OK, pick your strike.

Union Pacific UNP $234

Has now been steadily moving higher, up 10% since my first mention of it in October. It should continue jaggedly higher over the next 12 months as we move to the NSC/UNP merger and consolidation. And then after that, hopefully comes several quarters of cost cutting and so forth to give a steady tailwind. UNP announced the filing of their merger application with regulators last week, totaling 9000 or so pages. Stock got a lift on that…things are moving along.

In sum, a stock I believe I’ll own for a long time. If you are options inclined, the 20 delta 60-90 day calls are reasonable choices for covered call selling although right now, the stock has some upward momentum so beware of a call write too close to the price.

Cooper Company

Symbol COO $82.17

I first mentioned the stock at $72, so up 15% since then. As result of the pressure being applied by (now three) activist shareholders, I tripled my position to nearly 7%…top three holding. As in BILL, this should be monitored as an active situation. Stock ran all the way up to $90 on activist news, then backed down to the current price. As a result, I do believe there is upside room for the stock, although if you take a position, maybe not load up the boat. Again, risk/reward shifts once these things move higher.

BP and HON

BP has a new CEO and announced another division divestiture. Both stocks continue to be “show me” stocks among investors, but the thesis on both remain the same.

New thoughts worth mentioning

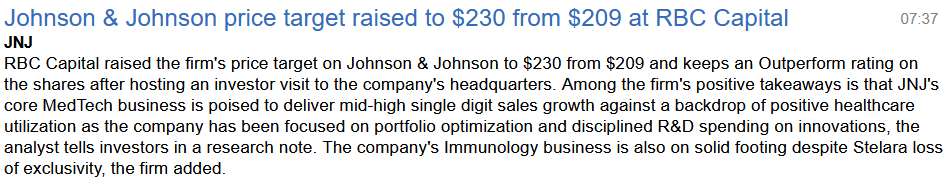

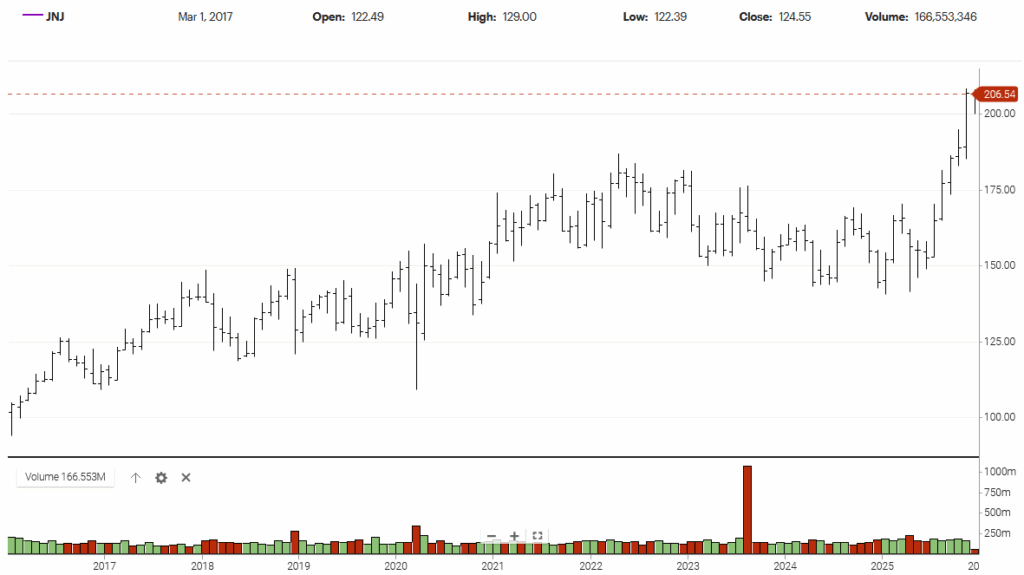

Johnson and Johnson

Symbol: JNJ $208.50

This is a stock I’ve owned, on and off, for most of my life. From time to time, it disappoints, but those disappointments are managed and the stock moves forward. The 10-year chart is instructive:

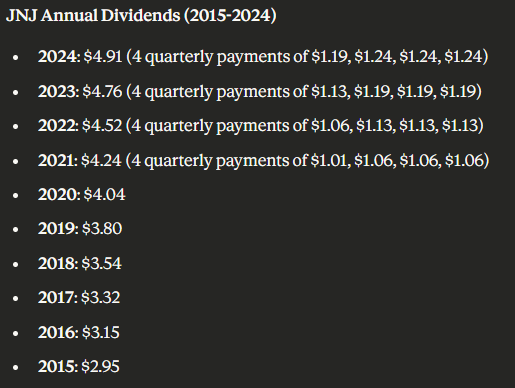

Dividends increase over time:

I think we all need some positions that are more or less permanent. Not that anything is not for sale, but in tough markets, stocks like this provide a comforting anchor and tend to perform relatively better. At its core, the business at JNJ is managed very well.

Here, remember our over riding goal is to help you grow your net worth and JNJ is exactly the type of exposure that helps do that. It’s had a good run recently, you could wait for the stock to back down. I think with JNJ, a good strategy is to simply wait for a downdraft in the stock and add to your position from time to time. Meanwhile, the latest analyst call offers upside potential, although the consensus call is “fairly valued.”